Note: this is a summary only and business owners should seek formal guidance about the tax implications of business structure in Australia.

If you’re considering setting up your business in Australia – or already have – then it’s important to understand that how you operate here can have some significant tax implications.

Setting up in Australia

Typically a foreign-owned business may establish operations in Australia in one of two ways:

- As a branch of a foreign company; or

- A wholly owned subsidiary of a foreign company.

Generally speaking, there is no significant relative advantage or disadvantage of either method for Australian tax purposes, as both are subject to transfer pricing issues and are required to file an Australian tax return.

Having said, if you operate as a branch, you are in a world of uncertainty as to how the branch is taxed in Australia. At the moment, the Government is undertaking a review in this area and a recommendation report from the Board of Taxation is due to release in April 2013.

What is a branch?

Do you know a foreign firm may be liable to pay taxes in Australia for sending its employees to work on projects without a physical office or traditional concept branch in Australia?

It is not uncommon to be engaged in assisting Australian projects for specialist or one off assignment involving a building site or construction or installation project.

Depending on the length of the project and also the existence of double tax treaty, the project itself may trigger a notional branch or a tax permanent establishment. Once a permanent establishment is created, the ATO has the right to tax the profit you derive as a foreign firm from the project.

Further, various employment taxes may be applicable to the foreign employees such as PAYG withholding, superannuation, Workcover and payroll tax although certain exemptions are available.

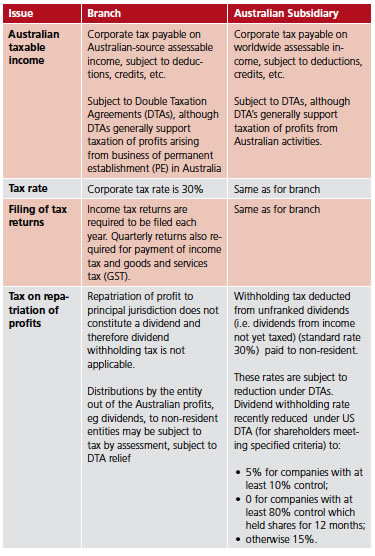

What are the key tax considerations for a branch vs a subsidiary?

The table below outlines the similarities and differences in tax treatment of a branch compared to a subsidiary:

More Information

Australia’s foreign tax law is inherently complex and we strongly advise that professional advice is sought when determining how to set up a presence here. For a more in-depth analysis of the tax treatment comparison, please contact Matt Zhou on 02 9957 4033.

Last updated November 2012. This factsheet is provided for information purposes only and is correct at the time of publishing. It should not be used in place of advice from your accountant. Please contact us on 02 9957 4033 to discuss your specific circumstances.